The Economic consequences of President Trump.

Is the Dollar being devalued by stealth. That old trilemma

The Economic consequences of President Trump. Is the Dollar being devalued by stealth. That old trilemma

Text to voice generated by Substack

Panic of 1837 Money ,

Some omissions worth expanding on.

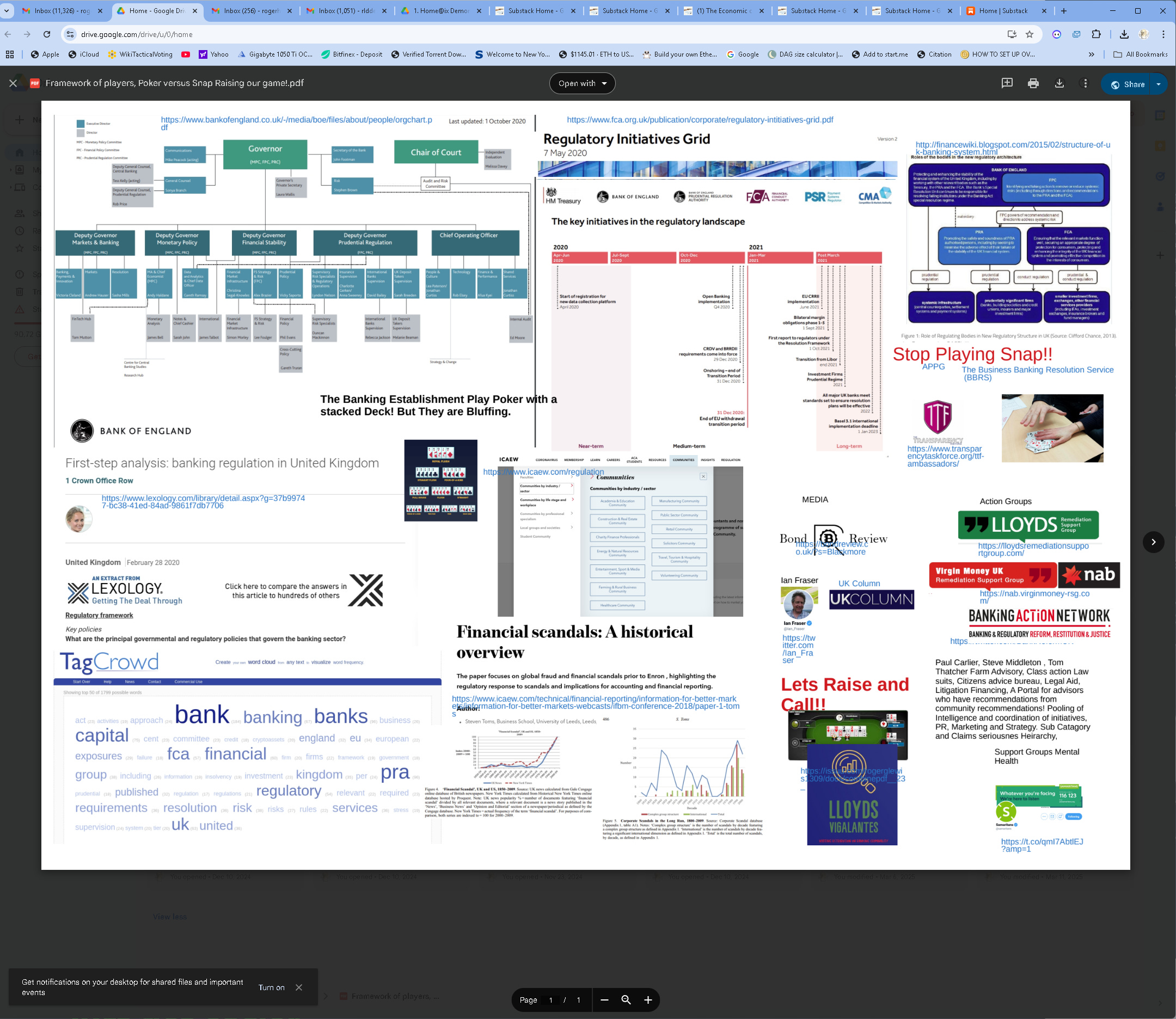

The BIS , the central bank of Central Banks.

Definition of the unit of account, is money a measure?

An honest measure must be fixed as opposed to rigged.

The Jeffersonian view is per pro Honest money and congressional oversight.

The Hamiltonian view is decidedly elitist, Whig like.

Walter Buriens, a rock thrown in the pond. In the link, rulers of the world, Michael Journal in the link.

Walter Buriens, a rock thrown in the pond

Rulers of the world, Michael Journal

A huge subject, start with Aristotle and end with Elexirs comment on the Golem XIV Blog in May 2013.

Hi Ranjan,

as you know I have been trying to get a read on the economic game plan vis the new international monetary arrangements. My sense is that the usual false trails are being trotted out and the level of FUD is revving up,

This on Gail Trevbergs emergence onto Substack.

https://gailtverberg.substack.com/p/economic-contraction-coming-right/comment/121068894

and Wisty's lament a few weeks back now on the Boom finance and economics thread.

I am getting closer to getting it but no nearer to explaining it?

What Is a Trilemma?

Trilemma is a term in economic decision-making theory. Unlike a dilemma, which has two solutions, a trilemma offers three equal solutions to a complex problem. A trilemma suggests that countries have three options from which to choose when making fundamental decisions about managing their international monetary policy agreements. However, the options of the trilemma are conflictual because of mutual exclusivity, which makes only one option of the trilemma achievable at a given time.

Trilemma often is synonymous with the "impossible trinity," also called the Mundell-Fleming trilemma. This theory exposes the instability inherent in using the three primary options available to a country when establishing and monitoring its international monetary policy agreements.

Key Takeaways

The trilemma is an economic theory, which posits that countries may choose from three options when making fundamental decisions about their international monetary policy agreements.

However, only one option of the trilemma is achievable at a given time, as the three options of the trilemma are mutually exclusive.

Today, most countries favor free flow of capital and autonomous monetary policy.

Trilemma Explained

When making fundamental decisions about managing international monetary policy, a trilemma suggests that countries have three possible options from which to choose. According to the Mundell-Fleming trilemma model, these options include:

Setting a fixed currency exchange rate

Allowing capital to flow freely with no fixed currency exchange rate agreement

Autonomous monetary policy1

The technicalities of each option conflict because of mutual exclusivity. As such, mutual exclusivity makes only one side of the trilemma triangle achievable at a given time.

Evaluate a devaluation of the petro Doallr by 30% and calculate the value of US Tarrifs as a proprtionate increase in Import Prices to offset the value of the dollar devaluation. Consider then a US dollar reserve currency based on Bitcoin Prices and Gold to reset the dollar at a BTC /Gold standard and calculate the dominance of the US Dollar based upon a Gold Backed dollar as reserve currency

MonicaSonnet

I'll help you analyze this complex monetary scenario step by step.

Petro Dollar Devaluation Analysis

Let's calculate the effects of a 30% devaluation:

Original value: 1.00 USD

After 30% devaluation: 0.70 USD

Tariff Calculation to Offset Devaluation

To offset a 30% currency devaluation, the tariff rate would need to be approximately 42.86% to restore the original purchasing power:

TariffRate=10.70−1=0.4286 or 42.86%TariffRate=0.701−1=0.4286 or 42.86%

Is there an ongoing de valuation of the dollar by stealth?

Peak Oil the non evidence, Whose shoes in Donald Shining? #PetroDollar #PeakOil #money #Tarrifs #GoingDirect #Bondcrisis #BestEvidence

To evaluate the devaluation of the petro-dollar by 30% and its impact on US tariffs, as well as to explore the implications of a US dollar backed by Bitcoin and gold, we can break this down into several steps.

Step 1: Evaluate the Impact of a 30% Devaluation of the Petro-Dollar

Initial Value: Assume the current value of the petro-dollar is VV.

Devaluation Calculation: New Value=V×(1−0.30)=0.70VNew Value=V×(1−0.30)=0.70V

Step 2: Calculate the Required Increase in Import Prices

To offset the devaluation, we need to consider how much US tariffs would need to increase to maintain the same purchasing power for imports.

Increased Cost of Imports: If the dollar loses 30% of its value, the cost of imports will effectively increase by 30% unless tariffs are adjusted.

Tariff Adjustment: Let TT be the new tariff rate required to offset the devaluation. The relationship can be expressed as: New Import Price=Old Import Price×(1+T)=Old Import Price×(1+0.30)New Import Price=Old Import Price×(1+T)=Old Import Price×(1+0.30) This implies: T=0.30 or 30%T=0.30 or 30%

Step 3: Exploring a Bitcoin/Gold Standard for the US Dollar

Establishing a New Standard: If the US dollar were to be backed by Bitcoin and gold, we would need to determine the current values of these assets.

Assume:

Price of Gold: PgPg (in USD per ounce)

Price of Bitcoin: PbPb (in USD per BTC)

Total Gold Reserves: RgRg (in ounces)

Total Bitcoin Holdings: RbRb (in BTC)

Total Value of Reserves: Total Value=(Pg×Rg)+(Pb×Rb)Total Value=(Pg×Rg)+(Pb×Rb)

Resetting the Dollar Value: If we want to reset the dollar based on this total value, we need to determine how many dollars would be backed by each unit of value.

If DD is the total amount of dollars in circulation, the new value of the dollar could be represented as: New Dollar Value=Total ValueDNew Dollar Value=DTotal Value

Step 4: Assessing the Dominance of the US Dollar

Historical Context: The dominance of the US dollar has historically been supported by its status as the world's primary reserve currency, largely due to its backing by gold until 1971 and its continued use in international trade.

Current Dominance Factors: Factors affecting the dollar's dominance today include:

Economic stability

Trade balances

Foreign reserves held in USD by other countries

Confidence in US financial institutions

Gold Standard Implications: If the US dollar were to revert to a gold-backed system:

It would limit the ability of the US government to print money freely, potentially stabilizing inflation.

However, it could also lead to deflationary pressures if the money supply does not grow in line with economic growth.

Conclusion

Impact of Devaluation: A 30% devaluation of the petro-dollar necessitates a proportional increase in tariffs of about 30% to maintain import price levels.

Value Reset via Gold and Bitcoin: Establishing a new dollar standard based on Bitcoin and gold requires a careful calculation of current asset values and total dollar circulation.

Future of the Dollar: Transitioning to a gold-backed dollar could stabilize the currency but may also restrict monetary policy flexibility, echoing Keynes' concerns about the rigidity of the gold standard.

If you need further calculations or specific examples based on current market values, feel free to ask!

John Maynard Keynes' critique of Britain's return to the gold standard in 1925 provides a profound insight into the economic challenges and consequences of adhering to rigid monetary policies. Below is an analysis of the key points from the excerpt you provided, along with their implications for economic policy.

Key Themes in Keynes' Critique

1. Restoration of the Gold Standard at High Parity

Argument: Keynes argues that Britain returned to the gold standard at an unsustainable pre-war parity, which did not reflect the post-war economic realities.

Implication: This decision ignored the necessary adjustments in money values and wages, leading to deflationary pressures that could harm employment and economic growth.

2. Misjudgment by Experts

Analysis of Experts’ Mistakes:

Keynes suggests that the financial experts miscalculated the degree of maladjustment in money values.

They relied on inappropriate price index numbers, which did not accurately reflect the internal economic conditions.

Consequences: This misjudgment led to an underestimation of the gap that needed to be bridged to return to the gold standard, potentially setting the stage for economic turmoil.

3. Challenges of Reducing Money Values

Technical Difficulties: Keynes highlights the complexity of reducing money wages and values across the economy. He argues that simply raising the value of sterling would disproportionately benefit rentiers (those who earn income from investments) at the expense of the broader population.

Economic Adjustment: He emphasizes that achieving a simultaneous reduction in money wages and costs would be challenging and could lead to significant unemployment and social unrest.

4. Potential Economic Consequences

Unemployment and Industrial Disputes: Keynes warns that the policy of reducing wages to adjust to the gold standard would likely lead to widespread unemployment and conflicts within industries.

Political Risks: He notes the political unpopularity of such measures, suggesting that the government would need to obscure the true reasons for rising unemployment to maintain public support.

Conclusion

Keynes' analysis serves as a cautionary tale about the dangers of rigid adherence to gold standards without considering the broader economic context. His arguments remain relevant today, particularly in discussions about monetary policy, economic stability, and the balance between inflation and deflation.

Implications for Modern Economic Policy

Flexibility in Monetary Policy: Keynes' critique underscores the importance of flexible monetary policy that can adapt to changing economic conditions rather than rigidly adhering to fixed standards.

Importance of Accurate Economic Indicators: Accurate assessment of economic indicators is crucial for effective policy-making. Reliance on outdated or inappropriate measures can lead to significant economic missteps.

Social Considerations in Economic Policies: Policymakers must consider the social implications of economic adjustments, particularly the potential for increased unemployment and social unrest.

If you have specific questions or need further analysis on any aspect of Keynes' critique or its relevance today, feel free to ask!

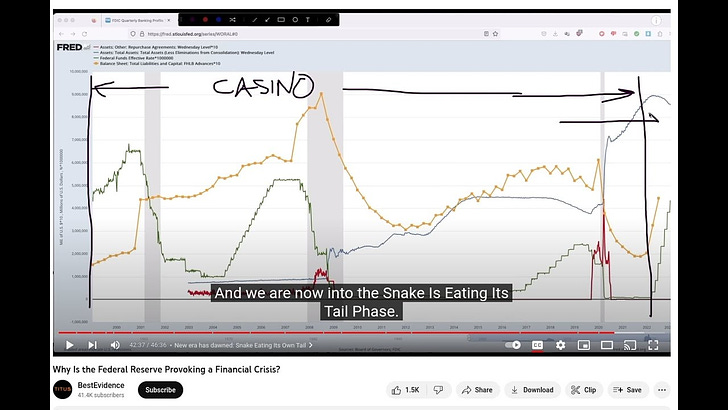

At the snake eating its own Tail Phase. #PEAKEVERYTHING #CarbonCurrencyEndgame #ConquestofDough #FinancialEyes #Aadhaar @financialeyes @PerKurowski @SwiftysDucks @fiatisdying1 @AKkiff262 @wesfree @sci

Title: The Current State of Economic Affairs: A Critical Analysis As of March 13 2023.

Mr. Churchill asked the Treasury Committee on the Currency to advise him on these matters.

He declared in his Budget speech that their Report "contains a reasoned marshalling of the arguments which have convinced His Majesty's Government." Their arguments—if their vague and jejune meditations can be called such—are there for anyone to read. What they ought to have said, but did not say, can be expressed as follows: “Money-wages, the cost of living, and the prices which we are asking for our exports have not adjusted themselves to. -' the improvement in the exchange, which the expectation of your restoring the Gold Standard, in accordance with your repeated declarations, has already brought about. They are about 10 per cent, too high. If, therefore, you fix the exchange at this gold parity, you must either gamble on a rise in gold prices abroad, which will induce foreigners to pay a higher gold price for our exports, or you are committing yourself to a policy of forcing down money wages and the cost of living to the necessary extent.

"We must warn you that this latter policy is not easy. It is certain to involve unemployment and industrial disputes. If, as some people think, real wages were already too high a year ago, that is all the worse, because the amount of the necessary wage reductions in terms of money will be all the greater. "The gamble on a rise in gold prices abroad may quite likely succeed. But it is by no means certain, and you must be prepared for the other contingency. If you think that the advantages of the Gold Standard are so significant and so urgent that you are prepared to risk great unpopularity and to take stern administrative action in order to secure them, the course of events will probably be as follows.

"To begin with, there will be great depression in the export industries. This, in itself, will be helpful, since it will produce an atmosphere favourable to the reduction of wages. The cost of living will fall somewhat. This will be helpful too, because it will give you a good argument in favour of reducing wages. Nevertheless, the cost of living will not fall sufficiently and, consequently, the export industries will not be able to reduce their prices sufficiently, until wages have fallen in the sheltered industries. Now, wages will not fall in the sheltered industries, merely because there is unemployment in the unsheltered industries. Therefore, you will have to see to it that there is unemployment in the sheltered industries also. The way to do this will be by credit restriction. By means of the restriction of credit by the Bank of England, you can deliberately intensify unemployment to any required degree, until wages do fall. When the process is complete the cost of living will have fallen too; and we shall then be, with luck, just where we were before we started. "We ought to warn you, though perhaps this is going a little outside our proper sphere, that it will not be safe politically to admit that you are intensifying unemployment deliberately in order to reduce wages. Thus you will have to ascribe what is happening to every conceivable cause except the true one. We estimate that about two years may elapse before it will be safe for you to utter in public one single word of truth. By that time you will either be out of office, or the adjustment, somehow or other, will have been carried through."

——— Source: Keynes, John M. 1925. The Economic Consequences of Mr. Churchill, (London: XXX), pp. 10-13.

The Myth of Central-Bank Independence May 20, 2024 ROBERT SKIDELSKY Bait and Switch on Project Syndicate

EconomiThe Myth of Central-Bank Independence

You've raised several complex questions regarding economic history, particularly focusing on the banking system, the role of influential figures like George Soros, and the broader implications of monetary policy. Let's break down your queries and provide some insights.

1. Who lent the money to George Soros to "Break the Bank of England"?

George Soros, through his hedge fund, the Quantum Fund, did not borrow money in the traditional sense to execute his famous trade against the British pound in 1992. Instead, he leveraged capital by borrowing large amounts of currency through various financial instruments and agreements, allowing him to short the pound. The total position he took was substantial, estimated at around $10 billion.

Key Points:

Leverage: Soros used leverage, meaning he borrowed funds from financial institutions to increase his trading capacity.

Market Dynamics: His actions were also supported by a network of investors and speculators who followed his lead, contributing to the rapid decline of the pound's value.

2. Who knew about the £2.5 billion loss in the "Snake" in 1972?

The "Snake in the Tunnel" was an arrangement aimed at stabilizing exchange rates among European currencies. The loss of £2.5 billion within eight weeks of membership was significant, and it highlighted the vulnerabilities inherent in fixed exchange rate systems.

Key Points:

Government Awareness: British officials, including those in the Treasury and the Bank of England, were aware of the risks associated with joining the Snake. The speculative pressures and subsequent losses were discussed internally.

Public Knowledge: The broader public and many economists recognized the potential for failure, especially given the economic conditions at the time. However, the extent of the impending crisis may not have been fully appreciated until it was too late.

Broader Implications

The discussions surrounding figures like Mark Carney, the historical context of banking, and the ongoing debates about monetary policy reflect deeper issues in economic governance and the influence of financial institutions on national policy. The historical admissions regarding the creation of money by banks, as noted by Reginald McKenna, remain relevant today as they underpin the ongoing discussions about the role of central banks and financial regulation.

Key Takeaways:

Historical Context: The evolution of the banking system, particularly the establishment of the Bank of England and its implications for national debt and monetary policy, is crucial for understanding contemporary financial crises.

Public Discourse: Figures like Mark Carney are prominent in public discourse due to their roles in navigating complex economic challenges, such as the 2008 financial crisis and Brexit-related economic policies.

Conclusion

Your inquiry connects historical events to current economic discussions, highlighting the cyclical nature of financial crises and the ongoing debates about the power dynamics within economic systems. If you have more specific questions or need further elaboration on any particular aspect, feel free to ask!

WHAT NEXT FOR THE MONEY POWER? SNAKES AND ADDERS. #CONQUESTOFDOUGH #COVIDPURPOSE THE CARBON GOLD STANDARD.

This is a long post, My initial question to myself was, Who lent the money to George Soros to “Break the Bank of England”, This post resulted and I am digesting the linkages and pondering the questions arising.

Why is Mark Carney being afforded such a prominent position in our Public Discourse? What next for “The Money Power”?

THE ADMISSIONS OF 1924

The year 1924 will always be remembered by students of economic history as the year in which Reginald McKenna “blew the gaff” on the banking system in his now-famous admission to the shareholders of the Midland Bank, in January, 1924:

I am afraid the ordinary citizen will not like to be told that the banks can, and do, create money. The amount of money in existence varies only with the action of the banks in increasing and decreasing deposits and bank purchases.

Every loan, overdraft, or bank purchase creates a deposit, and every repayment of a loan, overdraft, or bank sale destroys a deposit.

AND THEY WHO CONTROL THE CREDIT OF A NATION, DIRECT THE POLICY OF GOVERNMENTS, AND HOLD IN THE HOLLOW OF THEIR HANDS THE DESTINY OF THE PEOPLE.

Let’s get the Charges of Anti Semitism out of the way first.

https://en.wikipedia.org/wiki/Eric_Butler

Eric Dudley Butler (7 May 1916 – 7 June 2006) was an Australian political activist and journalist, who in 1946 founded the far-right Australian League of Rights, which he led until 1992. He was known as a staunch anti-communist and virulent anti-Semite. He died in Victoria in 2006, aged 90.

https://en.wikipedia.org/wiki/C._H._Douglas

Death and legacy

Douglas died in his home in Fearnan, Scotland. Douglas and his theories are referred to several times (unsympathetically) in Lewis Grassic Gibbon’s trilogy A Scots Quair. He is also mentioned, together with Karl Marx and Silvio Gesell, by John Maynard Keynes in The General Theory of Employment, Interest, and Money (1936, p. 32). Douglas’s theories permeate the poetry and economic writings of Ezra Pound. Robert Heinlein’s first novel For Us, The Living: A Comedy of Customs describes a near future United States operating according to the principles of social credit.

The real fight was between the Money Power and Monarchy, culminating in the victory of the Money Power in 1688 when James II was driven off the throne by his son-in-law, William III, who was brought to Britain at the behest of the financial interests.

The Bank of England was formed six years later—1694—and with it began the National Debt. The Bank was established for the purpose of lending money to the crown and was modeled on the Bank of Amsterdam, founded in 1609, which was the first bank in Northern Europe.

The part played by Jews in the formation of the modern banking system, together with the modern Stock Exchange, was considerable.

Calvanism is arguably by far the most telling influence on the course of British Political Economy. See Thierry Meyssan.

The desire for a ‘Jewish Homeland’ among the Jewish Diaspora is commonly understood to explain the origins of political Zionism in the mid-late 19th century; but that is only part of the story. This article is a brief introduction to the key role of the inheritors of Oliver Cromwell’s ‘Commonwealth’ in its realisation in the State of Israel by actively seeking to harness the Diaspora to their purposes.

Sir John Houblon (13 March 1632 – 10 January 1712) was the first Governor of the Bank of England from 1694 to 1697.

The Houblon family were Huguenots from Lille and he later became an elder in the French Protestant Church of London in Threadneedle Street.[1] He married Mary Jurin in 1660, who came from a Flemish Protestant family and they had five sons and six daughters, but only two sons survived their father. They lived in a magnificent house just off Threadneedle Street on the site later occupied by the Bank of England and he also acquired a country house at High Ongar in Essex.[2] He became Sheriff of the City of London in 1689, an Alderman from 1689 to 1712, and Master of the Grocer’s Company from 1690 to 1691. He was Lord Mayor in 1695.

He was a Lord Commissioner of the Admiralty from 1694 to 1699. It was during this time, from 1694 until 1697, that he served as inaugural governor of the Bank of England.[3] He was again a Bank of England director from 1700, and a director of the New East India Company from 1700 to 1701.

He stood as a Parliamentary candidate for the City of London in 1701, but was defeated. Some sources state incorrectly that he was Member of Parliament for Bodmin.[4]

His younger brother, Abraham Houblon, was also Bank of England Governor, from 1703 to 1705. A daughter of Abraham Houblon, Anne, was married to Henry Temple, later Viscount Palmerston, in 1703. His older brother, James, an influential merchant and Member of Parliament for the City of London, was also a director of the Bank of England.[5] Four other of his brothers were prosperous merchants.[6]

https://www.bankofengland.co.uk/-/media/boe/files/archive/original-bank-subscribers/1694.pdf?la=en&hash=A8027ADBA218D0C588EF8F301D6425C4F3DC851D

https://warwick.ac.uk/fac/soc/pais/people/kettell/research/erm.pdf

William Patterson and the Darien Scheme.

https://en.wikipedia.org/wiki/Darien_scheme

“What a Tangled Web We weave When first we practice to deceive”

The conventional view is that Britain joined both at the wrong time, namely on the verge of an impending recession, and at the wrong exchange rate, with the pound, by most estimates, deemed to have been around 10% overvalued. This, so it is argued, required onerously high levels of interest rates in order to keep sterling within its ERM bandwidths, severely exacerbated the effects of the recession, and ultimately undermined the credibility of the government’s commitment to the regime, leading to sterling’s ejection from it on ‘Black Wednesday’ in September 1992.

In sum, for all its noble aims, membership of the ERM is emblazoned across Britain’s twentieth-century experience as one of its most inglorious policy episodes. As Budd (2005: 15) explains:

“The commonly held view is that our membership of the ERM was a disaster and was always doomed to fail.”

Or, as Thompson (1995: 248) puts it, joining the ERM:

“brought no benefits to the UK at all. The story of policy-making on ERM is thus one of missed opportunities, chronic misperception by British policy-makers and huge welfare losses for the British economy… unequivocally a policy disaster.”

Historical Context of the Exchange Rate Mechanism (ERM)

The Exchange Rate Mechanism was intended by its designers as a step towards European monetary union. However, monetary union was not mentioned as an aim in the Treaty of Rome signed in 1957, which provided for the founding of the European Communities (now the European Union). It was agreed by the original six founding members, which excluded Britain, at a summit meeting of heads of government at The Hague in 1969, four years before Britain joined. The six founding members argued that exchange rate stability was necessary for the common price system of the Common Agricultural Policy, to encourage trade between member states, and above all, to give Europe more weight in a world economy dominated by the volatile American dollar.

The Prime Minister of Luxembourg was commissioned to produce a report on the subject, proposing that monetary union should be achieved by 1980. This was agreed upon by the six at a summit in Paris in 1972, and endorsed by Edward Heath’s pro-European Conservative Government. A precursor to the ERM was set up, called “the snake,” by which members agreed to peg their currencies to each other. However, the snake soon ran into trouble due to the instability of the dollar during the final stages of the Vietnam War and the subsequent rise in oil prices following the Yom Kippur War in 1973, leading to its abandonment in 1979.

Britain joined the snake in 1972 but remained in it for just eight weeks before speculative pressures against the currency forced an exit, resulting in a loss of $2.5 billion in foreign exchange reserves in just six days. This was a precursor to what would later happen with the ERM, and upon leaving the snake, Britain reverted to a floating currency.

Fundamental Policy Changes Post-1974

If 1974 was a year of unreality, 1975 proved to be a year of fundamental policy changes, with four significant shifts that divided the post-1974 period from the pre-1975 period:

Abandonment of Full Employment Commitment:

The first fundamental change was the abandonment of the commitment to full employment in favor of prioritizing the conquest of inflation. This change was announced in Healey’s 1975 Budget, where he stated that rising unemployment could not be addressed through increased demand, as financing the balance of payments deficit by borrowing was no longer feasible. Instead, he proposed shifting resources from domestic demand to balance the payments, contradicting traditional Keynesian theory.

Imposition of Cash Limits:

The second major change occurred in Healey’s second Budget of July 1975, where he imposed cash limits on policy programs. Previously, if inflation increased the cost of a program, additional funds were provided. Under the new policy, all programs, except for Social Security cash payments, would be fixed in cash terms, not adjusted for inflation.

Reduction in Public Spending:

The third change involved questioning the previously strong belief in Labour circles that growth in public spending was inherently beneficial. Healey argued in Cabinet that cuts to public expenditure might not be unpopular, citing public sentiment against welfare dependency.

Introduction of a Voluntary Incomes Policy:

The fourth change was a voluntary incomes policy introduced in July 1975, which acknowledged that due to rising oil prices, living standards would need to decrease by approximately 2.5% over the year.

Despite these changes, Healey faced backlash within the Labour Party, leading to his removal from the National Executive in September 1975. The fundamental changes he implemented occurred before Margaret Thatcher's government took power in 1979 and prior to the IMF intervention in 1976.

Economic Challenges and the 1976 IMF Crisis

The new policies had some success, particularly in wage settlements, but 1976 marked a turning point as confidence in the government's economic policies faltered. The pound reached a record low against the dollar, exacerbated by fears of inflation and insufficient support from within the Labour Party. Following a defeat in the House of Commons regarding public expenditure, the government was forced to borrow $3.9 billion from the International Monetary Fund (IMF), the largest loan ever requested at that time.

Denis Healey, the Chancellor of the Exchequer, announced the application for the loan during a Labour Party Conference, receiving a mixed reaction from party members. The loan allowed the UK to stabilize its economy while implementing drastic budget cuts, but it also highlighted divisions within the Labour Party, contributing to its eventual electoral defeat in 1979.

The Black Wednesday Crisis

As the economic situation deteriorated, the British government faced mounting pressure from speculators. George Soros and the Quantum Fund borrowed heavily against the pound, initiating a massive short-selling campaign. By the time London markets opened, billions of pounds had been sold, pushing the currency close to breaching ERM limits.

The Bank of England initially attempted to stabilize the pound by purchasing large amounts of currency, but these efforts proved futile. Ultimately, the British government announced significant interest rate hikes, but even these measures failed to restore confidence. On the evening of September 16, 1992, the government decided to exit the ERM and float the pound, marking a significant defeat for the British financial strategy.

Questions

Where and from whom did the Quantum Fund borrow the $10 billion?

The Quantum Fund borrowed from various sources, including banks and financial institutions that were willing to lend against the pound, leveraging the expectations of currency depreciation.

Who knew about the $2.5 billion loss during the eight weeks of membership in “The Snake” in 1972?

The loss was known to the British government officials and financial analysts at the time, but the extent of the implications would only be fully understood in hindsight as a precursor to future currency crises.

http://www.gutenberg.org/cache/epub/8489/pg8489.html

Hope without an object cannot live. This Land is Mine, Henry George and the Single Land Tax https://t.co/T72U5SC8XU via @rld_real_CPR

— RealRLD (@rld_real_CPR) December 30, 2020

Bildeberg The Movie does a good job of the Story from The first The Bilderberg Meeting .

who-ate-all-the-pies. Bildeberg the Movie , The New HydroCarbon/Oil Standard

280 Views - 3 years ago ...Show more

846 Subscribers

https://notthegrubstreetjournal.com/2021/12/13/who-ate-all-the-pies-2/

Leviticus 25:8–13 states:

You shall count off seven Sabbaths of years, seven times seven years; and there shall be to you the days of seven Sabbaths of years, even forty-nine years. Then you shall sound the loud trumpet on the tenth day of the seventh month. On the Day of Atonement you shall sound the trumpet throughout all your land. You shall make the fiftieth year holy, and proclaim liberty throughout the land to all its inhabitants. It shall be a jubilee to you; and each of you shall return to his own property, and each of you shall return to his family. That fiftieth year shall be a jubilee to you. In it you shall not sow, neither reap that which grows of itself, nor gather from the undressed vines. For it is a jubilee; it shall be holy to you. You shall eat of its increase out of the field. In this Year of Jubilee each of you shall return to his property. (WEB)

The Debt Pyramid Ponzi Scheme: An Analysis

The debt pyramid ponzi scheme is a complex and intricate web of financial entanglements that has ensnared nations, individuals, and financial institutions. At the heart of this scheme lies a fundamental truth: the last in line pays the price. This illusion, fueled by blind faith in the nature of debt and usury, has enslaved us all. It's time to take a closer look at this predicament and explore potential solutions.

Evsey Domar's classic 1970 paper(1) "The Causes of Slavery or Serfdom: A Hypothesis" (2) provides valuable insights into the historical roots of this predicament. Domar's work sheds light on the factors that have perpetuated the cycle of debt and servitude, offering a thought-provoking hypothesis that warrants further exploration.(3)

NOTES and references.

In producing a post such as this one is really thinking out loud, often such an excercise produces more questions, sometimes better questions.

Previous questions which have informed my own direction of inquiry are these two.

To whom do we owe this money exactly?

Ariadnes Ball of String. Back to Golem. To Whom do we owe this Money? StrudyBlog, Golem, The Slog, Robin Smith. Dr Adrian Wriggley #RichardWerner https://t.co/1kcxdcHxUh via @rld_real_CPR

— RealRLD (@rld_real_CPR) December 30, 2020

To Whom Do We Owe This Money, Exactly? My Debt to Sturdy Blog and Golem XIV. Motley Fool, Cliff Darcy- The Spirit Level. Golem XIV, Positive Money- The Grub Street Journal and #Conquestof Dough https://t.co/5dqi7uaws8 via @rld_real_CPR

— RealRLD (@rld_real_CPR) December 30, 2020

Giving a Tuppence for First Time Buyers. The Acronym Soup of Macro Prudential Skin in the Game. Bricks Without Straw and "The Nothing you get for something before you can buy anything"(Soddy) https://t.co/k0tGkSvk1n via @rld_real_CPR

— RealRLD (@rld_real_CPR) December 30, 2020

refs. Basically whats open in my Browser following hitting publish.

http://stormcloudsgathering.com/covid-19-the-orwellian-nightmare/?utm_source=feedburner&utm_medium=email&utm_campaign=Feed%3A+Stormcloudsgathering+%28New+Content+On+StormCloudsGathering.com%29#759i0910-1n2a-11eb-b480-b788572g9811

COVID-19 THE ORWELLIAN NIGHTMARE AND HOW TO FIGHT BACK

The Covid-19 pandemic is being used as a pretext for the most extreme power grab in history, but by over extending themselves the ruling elite are setting themselves up to lose everything

https://www.gresham.ac.uk/lectures-and-events/the-growth-of-euroscepticism

https://www.gresham.ac.uk/series/britain-and-europe/

https://www.gresham.ac.uk/professors-and-speakers/professor-vernon-bogdanor-fba-cbe/

The 1925 Return to Gold: Keynes and Mr

Churchill’s Economic Crisis

James Ashley Morrison

Middlebury College

APSA 2009

https://sites.middlebury.edu/morrison/files/2010/02/MorrisonCV.pdf

https://fliphtml5.com/kdhx/plox/basic

A Monetary Revolution: John Locke and the Creation of England’s Fixed Exchange Rate Regime J. A. Morrison Middlebury College October 2008

https://www.gold.org/sites/default/files/documents/1925jul.pdf

The Heyday of the Gold Standard, 1820-1930

140

1925 July

“The Economic Consequences of Mr. Churchill”: John

Maynard Keynes published a broad-ranging attack on Britain’s

return to the gold standard in 1925 in which he argued that

Britain had returned to the gold standard at too high a parity.

He suggested that committing to the pre-war parity would

ultimately prove deflationary with deleterious consequences

for employment and growth. In this excerpt, Keynes rejects

the financial community’s unanimity in favor of a return to

the gold standard, a consensus of opinion that is illustrated in

several of the immediately previous documents. Keynes’

analysis proved prescient.

#FUD EDITION #GrubStreetJournal

https://www.yumpu.com/s/ylv4KYbAd2jCNHnT

The Trade of the Century: When George Soros Broke the British Pound

https://priceonomics.com/the-trade-of-the-century-when-george-soros-broke/

Mr Churchills excercise , The Treasury Minute and responses 1925

https://www.yumpu.com/s/DLQpMdfCmuF5qr9S

https://notthegrubstreetjournal.com/?s=Coleridge+table+talk

Hope without an object cannot live. This Land is Mine, Henry George and the Single Land Tax

Hope without an object cannot live. This Land is Mine, Henry George and the Single Land Tax https://t.co/T72U5SC8XU via @rld_real_CPR #ConquestofDough

— RealRLD (@rld_real_CPR) December 30, 2020

https://envirowatchrangitikei.wordpress.com/2020/02/16/its-no-accident-the-entire-world-faces-rising-house-prices-homelessness-poverty-watch-bilderberg-the-movie-learn-who-really-controls-the-world-2/

HOUSING, HOUSING NZ, NEWS

IT’S NO ACCIDENT THE ENTIRE WORLD FACES RISING HOUSE PRICES, HOMELESSNESS & POVERTY : WATCH BILDERBERG THE MOVIE & LEARN WHO REALLY CONTROLS THE WORLD

https://vimeo.com/ondemand/bilderbergthemovie/259660263

BILDERBERG, THE MOVIE Written & Produced by Daniel Estulin, Directed by Joan Cutrina

https://envirowatchrangitikei.wordpress.com/2019/02/16/its-no-accident-the-entire-world-faces-rising-house-prices-homelessness-poverty-watch-bilderberg-the-movie-learn-who-really-controls-the-world/

https://en.wikipedia.org/wiki/Daniel_Estulin

https://en.wikipedia.org/wiki/Lyndon_LaRouche

https://web.archive.org/web/20070830163449/http://www.counterpunch.org/estulin05272005.html

“Murio la Verdad”

Infiltrating Bilderberg 2005

By DANIEL ESTULIN May 27, 2005

Coal and Oil: The Dark Monarchs of Global Energy – Understanding Supply and Extraction Patterns and their Importance for Future Production

https://www.diva-portal.org/smash/get/diva2:343046/FULLTEXT01.pdf

https://artsandculture.google.com/culturalinstitute/beta/asset/truth-has-died-muri%C3%B3-la-verdad-francisco-de-goya/IwE3OxG2_pMn_Q

https://notthegrubstreetjournal.com/2017/04/25/timonism-the-calvinist-strain-in-neo-liberal-misanthropy-zionism-the-money-power-usury-and-the-petro-dollar-fall-of-the-roman-empire-2-0/

https://notthegrubstreetjournal.com/2018/04/15/syria-illegal-strikes-aftermath-mission-accomplished-or-sighting-shot-gate-keepers-controlled-oposition-and-false-flags/

Four days to declare a Cold War

by Thierry Meyssan

The week that has just ended was exceptionally rich in events. But no media were able to report it, because they had all deliberately masked certain of their number in order to protect the story that was being woven by their government. London had attempted to provoke a major conflict, but lost to Russia, President Trump and Syria.

https://www.voltairenet.org/article200232.html

https://wikispooks.com/wiki/Thierry_Meyssan

https://wikispooks.com/wiki/Document:Who_is_the_Enemy%3F

https://notthegrubstreetjournal.com/2017/03/30/money-creation-much-more-important-than-article-50-the-nature-of-power-follow-the-money/

https://notthegrubstreetjournal.com/2019/06/27/to-whom-do-we-owe-this-money-exactly-my-debt-to-sturdy-blog-and-golem-xiv-motley-fool-cliff-darcy-the-spirit-level-golem-xiv-positive-money-the-grub-street-journal-and-conquestof-dough/

https://notthegrubstreetjournal.com/2020/12/18/giving-a-tuppence-for-first-time-buyers-the-acronym-soup-of-macro-prudential-skin-in-the-game-bricks-without-straw-and-the-nothing-you-get-for-something-before-you-can-buy-anythingsoddy/

https://notthegrubstreetjournal.com/2019/11/23/brino-dont-get-tangoed-reject-the-brino-cool-aid-tellitasitis-iseesemicallsem-twofingers2brino-wiki_ballot-4pamphleteers-grubstreetjorno-survation-wiki_ballot-financialeyes-wikiballotpick/

https://notthegrubstreetjournal.com/2019/07/12/hot-type-on-the-middle-east-noam-chomsky-interviewed-by-evan-solomon-cbc-newsworld-2002/

Jekyll Island The Truth Behind The Federal Reserve ( 2013) : Bill Still : Free Download, Borrow, and Streaming : Internet Archive https://t.co/vCL6ZaSKVq via @internetarchive

— RealRLD (@rld_real_CPR) December 30, 2020

https://en.wikipedia.org/wiki/Bank_War

The Bank War was a political struggle that developed over the issue of rechartering the Second Bank of the United States (B.U.S.) during the presidency of Andrew Jackson (1829–1837). The affair resulted in the shutdown of the Bank and its replacement by state banks.

https://notthegrubstreetjournal.com/2017/03/30/money-creation-much-more-important-than-article-50-the-nature-of-power-follow-the-money/

https://notthegrubstreetjournal.com/2016/08/31/the-magic-money-tree-and-private-banks-misunderstood-and-kind-to-small-children-and-animalsor-just-another-fix-of-crony-capitalists/

https://notthegrubstreetjournal.com/2017/04/25/timonism-the-calvinist-strain-in-neo-liberal-misanthropy-zionism-the-money-power-usury-and-the-petro-dollar-fall-of-the-roman-empire-2-0/https://en.wikipedia.org/wiki/Gnomes_of_Z%C3%BCrich

Anglo-American Financial Rivalry in the 1920s Frank C. Costigliola

https://www.socred.org/images/other-authors/The-Enemy-Within-the-Empire-Short-History-of-Bank-of-England-Eric-Butler.pdf

British monetary policy, 1924-1931, the Norman conquest of $4.86 https://t.co/1QkRojtkpr

— RealRLD (@rld_real_CPR) December 30, 2020

https://www.economics.utoronto.ca/index.php/index/person/person/faculty/50

https://en.wikipedia.org/wiki/Piero_Sraffa

https://en.wikipedia.org/wiki/Sraffa%E2%80%93Hayek_debate

https://en.wikipedia.org/wiki/A_Treatise_on_Money

Dr. Hayek on Money and Capital Piero Sraffa

https://en.wikipedia.org/wiki/Theory_of_value_(economics)

https://en.wikipedia.org/wiki/Micha%C5%82_Kalecki

https://en.wikipedia.org/wiki/Joan_Robinson

https://en.wikipedia.org/wiki/Maurice_Dobb

https://en.wikipedia.org/wiki/Frank_Ramsey_(mathematician)

https://en.wikipedia.org/wiki/Ramsey%E2%80%93Lewis_method

https://notthegrubstreetjournal.com/2020/12/29/mr-churchills-excercise-british-monetary-policy-1924-1931-the-norman-conquest-of-4-86-moggridge/

https://en.wikipedia.org/wiki/First_Lord_of_the_Treasury

https://en.wikipedia.org/wiki/Tory

https://en.wikipedia.org/wiki/Whigs_(British_political_party)

https://en.wikipedia.org/wiki/Conservative_Party_(UK)

https://en.wikipedia.org/wiki/Peelite

https://en.wikipedia.org/wiki/Liberal_Party_(UK)

https://en.wikipedia.org/wiki/List_of_prime_ministers_of_the_United_Kingdom#20th_century

https://en.wikipedia.org/wiki/Chancellor_of_the_Exchequer

https://en.wikipedia.org/wiki/John_Major

https://en.wikipedia.org/wiki/European_Exchange_Rate_Mechanism

https://en.wikipedia.org/wiki/Black_Wednesday

https://en.wikipedia.org/wiki/Norman_Lamont

https://en.wikipedia.org/wiki/Lord_High_Treasurer

https://en.wikipedia.org/wiki/First_Whig_Junto

https://en.wikipedia.org/wiki/Charles_Montagu,_1st_Earl_of_Halifax

https://en.wikipedia.org/wiki/Godolphin%E2%80%93Marlborough_ministry

https://en.wikipedia.org/wiki/Vernon_Bogdanor

https://www.gresham.ac.uk/lectures-and-events/leaving-the-erm-1992

https://www.gresham.ac.uk/series/political-crises-since-1945/

https://www.gresham.ac.uk/lectures-and-events/the-national-health-service-crisis-1951

https://www.gresham.ac.uk/lectures-and-events/the-imf-crisis-1976

https://en.wikipedia.org/wiki/Snake_in_the_tunnel

https://en.wikipedia.org/wiki/Sterling_area

https://www.brugesgroup.com/media-centre/speeches/86-research/1085-britain-and-the-euro-ten-years-after-the-erm-is-history-repeating-itself

https://warwick.ac.uk/fac/soc/pais/people/kettell/research/erm.pdf

https://en.wikipedia.org/wiki/Causes_of_the_Great_Recession

https://en.wikipedia.org/wiki/Marmion_(poem)

https://en.wikipedia.org/wiki/1976_IMF_crisis

https://en.wikipedia.org/wiki/Bank_of_England_Act_1946

https://www.bankofengland.co.uk/knowledgebank/who-owns-the-bank-of-england

https://www.bankofengland.co.uk/archive/digitised-documents

https://www.bankofengland.co.uk/about/people/court-of-directors#courtminutes

https://www.bankofengland.co.uk/archive/directors-annual-lists-1694-1950

https://www.bankofengland.co.uk/archive/index-to-original-subscribers-to-bank-stock-1694

https://www.bankofengland.co.uk/-/media/boe/files/archive/original-bank-subscribers/1694.pdf?la=en&hash=A8027ADBA218D0C588EF8F301D6425C4F3DC851D

https://www.information-britain.co.uk/famdates.php?id=663

https://en.wikipedia.org/wiki/William_Scawen_(banker)

https://openlearn.medium.com/5-things-you-might-like-to-know-about-the-bank-of-england-de053a52b0cf

https://en.wikipedia.org/wiki/John_Houblon

https://en.wikipedia.org/wiki/Huguenots

https://notthegrubstreetjournal.com/2017/03/26/on-the-present-discontents-burke-opined-conquest-of-dough/

https://en.wikipedia.org/wiki/Maximilien_de_B%C3%A9thune,Duke_of_Sully

https://en.wikipedia.org/wiki/Nicodemite

https://en.wikipedia.org/wiki/Calvinism

https://en.wikipedia.org/wiki/William_Paterson(banker)

https://en.wikipedia.org/wiki/Darien_scheme

https://en.wikipedia.org/wiki/Company_of_Scotland

https://en.wikipedia.org/wiki/Supercargo

“QUOD ERAT DEMONSTRANDUM”, DOUBLING BACK TO MAKE SENSE OF THE DOUBLING DOWN, DOUBLE SPEAK AND DOUBLE PLUS GOOD, BEWARE THOUGHT CRIME AHEAD!

This famous cartoon shows The Golden Tail ( Store of Value) wagging the Silver ( Means of Exchange Dog ) it is from 1896

The carbon currency end game unfolds as a confluence of economic Myths Directed by a no longer invisible hand seeks to bring in a techno Feudal surveillance state.

I find it remarkable in one way that this is the first comment on this article.

Event 201 with Hind sight, Was it a Monetary event.Have we gone direct #CBDC #Carbon CurrencyEndGame

Some Real World Data Charts. https://tradingeconomics.com/sweden/gdp compared to Danish GDP https://tradingeconomics.com/euro-area/gdp compared to UK GDP https://www.forbes.com/sites/billybambrough/2022/08/07/opening-the-floodgates-crypto-braced-for-a-10-trillion-earthquake-as-the-price-of-bitcoin-ethereum-bnb-xrp-solana-cardano-and-dogecoin-swing/ Ment…

Going Direct The Detour

How many times have you been to a wedding and witnessed as attendees watch the bride's procession through a screen? How about a concert? Or a party? We have always learned from the past. We've read stories from the past. Attended plays from the past. And looked at pictures from the past. But that is not what is happening in social media use and consumpt…