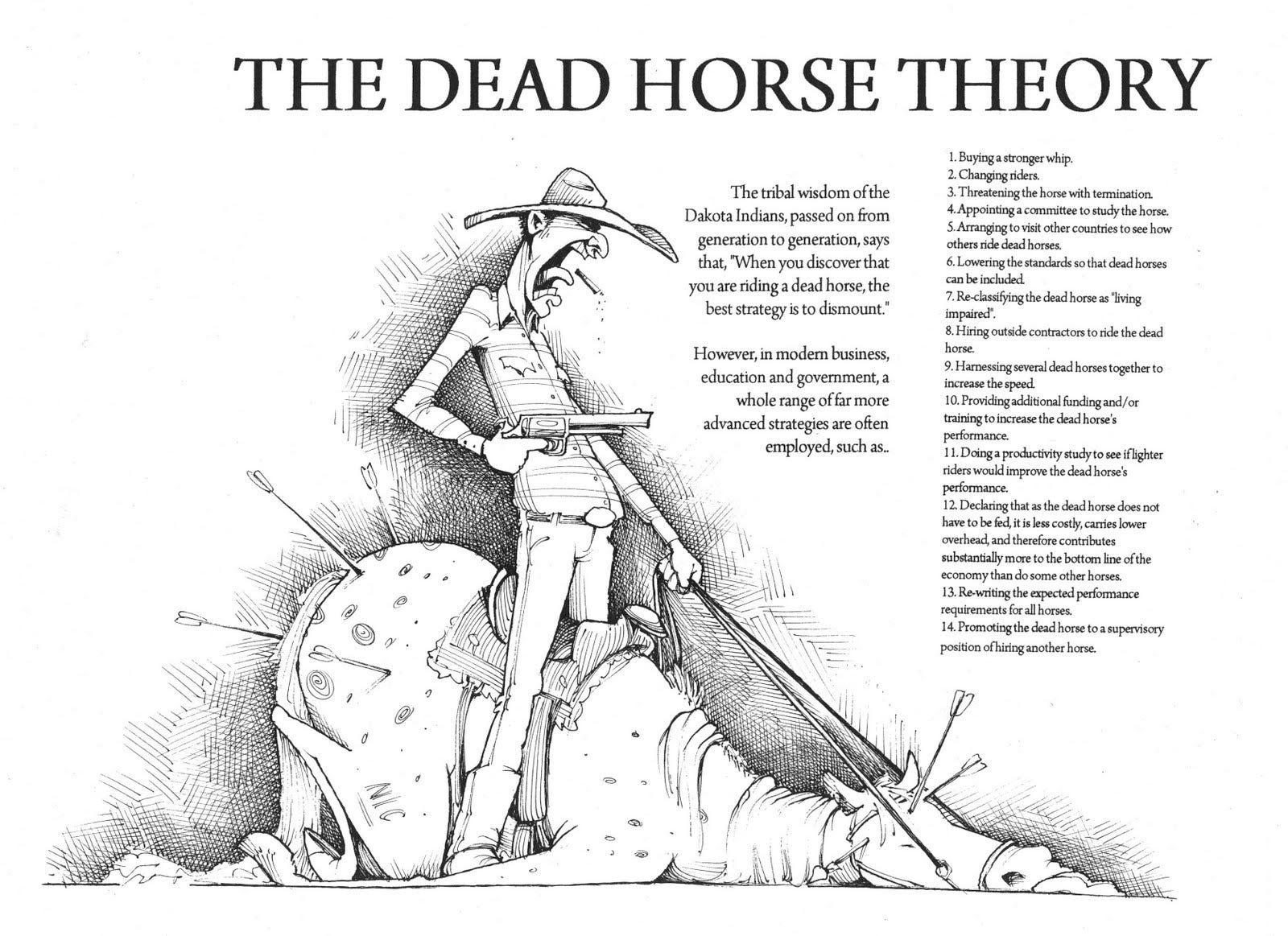

Stylized modelled theory and Empirical Evidence. Seeds of Proof.

Keep flogging the flogging of a dead horse approach.

September 23, 2013

Capitalist Dead Horse Flogs 99%

The term Flogging a Dead horse shouldn’t need any introduction. Whether Capitalism is a Golden Goose or a Dead horse may require some further explanation.

Capitalism is a New religion, The Free Market is the New Heaven and a belief in Capitalism is an unquestionable stance. Criticise Capitalism and you are declaring the Earth Flat, the Sun revolves around the Earth and are dangerously out of line.

”As Bakunin put it, property “is a god” and has “its metaphysics. It is the science of the bourgeois economists. Like any metaphysics, it is a sort of twilight, a compromise between truth and falsehood, with the latter benefiting from it. It seeks to give falsehood the appearance of truth and leads truth to falsehood.” [The Political Philosophy of Bakunin, p. 179]

http://en.wikibooks.org/wiki/Anarchist_FAQ/What_are_the_myths_of_capitalist_economics%3F

Two Discussion caught my Eye this past Week, One the Question of Minimum Wages and Mc Donalds and the Other a Film about Artists rights and the devaluing of Creative property due to digitisation.

June 7, 2018

Flogging the 99%. Keen explaining his reasons for pursuing his dynamic systems modelling with the importance of debt & money factored in . Is There a God of Markets

Keep flogging the flogging of a dead horse approach.

#302: At the end of modernity, part one

Posted on May 5, 2025

THE CONSEQUENCES OF COLLECTIVE SELF-DELUSION

As some readers will know, I recently chose to use a period of necessary travel to isolate myself, for a space, from all forms of purported “news” and “information”.

It is something that I can heartily recommend to anyone, even if it involves just a few hours spent fishing at a place where no fish are to be found.

During this period of reflection, I gained a much clearer perspective on how a chapter of instability masquerading as “modernity” will end, even if the basics – the unfolding failures of money and technology – were already apparent.

Whilst our understanding of these basics will continue to improve, the task now is to strengthen the correlation between the calculated and the experienced.

What is particularly striking is the contrast between the abundant evidence of economic contraction and a near-universal refusal to accept this reality.

In practical terms, this means that “modernity” will end, not gradually, but very rapidly indeed.

#303: At the end of modernity, part two

Posted on May 17, 2025

VANISHING POINTS, ANGLES OF CAPSIZE

There is a vanishing point in art, best illustrated by the way in which railway lines, though physically parallel, converge, through the effect of distance, towards a single point at the horizon.

There is, too, a vanishing angle in naval architecture. Though this is a complicated matter of waterplane areas, transverse metacentric heights and righting couples, its practical meaning is ‘that degree of list beyond which a vessel cannot roll back to the perpendicular’.

The global economy is now at – or, in some cases, beyond – some vanishing points and vanishing angles of its own.

Many cherished assumptions are being invalidated as economic growth ends, and contraction sets in. The tophamper of the financial system, seen as an aggregate weight of liabilities, has out-grown the underlying material economy to a point at which the moment of capsize is drawing ever nearer.

Representational art and naval architecture hold fascinations for many, and so, in its own way, does economic theory. But the great reality of our age is that the time available for theoretical development is fast running out.

The Scylla and Charybdis of our times are the tension between the impossibility of further economic growth and the near-total inability of society to accept and come to terms with this new reality.

Energy costs: the scary reality behind the headlines

9th February 2022 by Tim Morgan 1 Comment

For perfectly understandable reasons, public and media reactions to the surge in energy prices have concentrated almost exclusively on rises in the cost of domestic gas and electricity, and of filling up the family car with petrol or diesel.This, though, is to miss more than half the point, because the even bigger consequence of the energy supply squeeze is what it means for industry. It’s simply impossible to run a business without using energy.

The supply of food is just one example. Just as farmers need fuel to plant and harvest crops, suppliers of fertilisers and other agricultural inputs need energy to extract, process and deliver raw materials, and energy is needed, too, for the manufacture, servicing and maintenance of farming equipment. Food manufacturers need energy for processing and transport, and the supply chain from producers and distributors to retailers relies on it for everything from trucks to refrigeration.

Don’t be surprised, then, when rising energy costs show up in the weekly grocery bill.

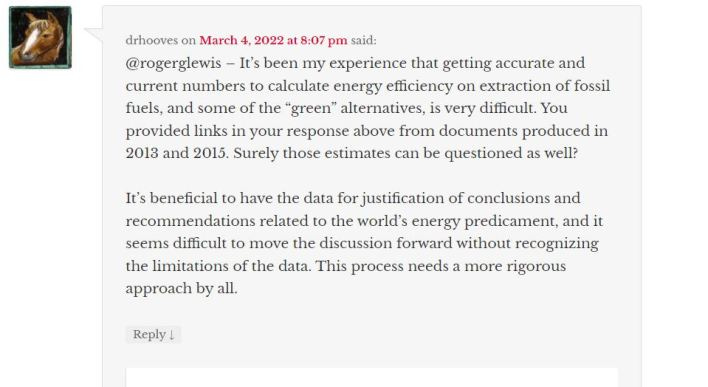

Roger G Lewis says

Dr. Morgan is quite right regarding how essential Energy is to a modern economy.

The price of energy production is of course logically connected to the available energy or Surplus Energy available for productive purposes within the real economy. This tautology is though only part of the story.

Before reaching the same conclusion that the inevitable age of surplus energy has arrived the Nature of the Debt-based model used in the creation of the money used as the measure of and currency for exchange in modern political economy must first be accounted for. A sensible explanation of the main contributory causes of the present difficulties faced by the Global economy particularly in the Post Fordist developed economies is assisted with a judicious application of Occam’s razor..

Dr Morgan says that “before the coronavirus crisis, Britain had been borrowing more than £4 for each £1 of “growth” whilst this is broadly correct the allocation of the debt, largely to the FInancialised sector for speculation on non-productive purposes such as Share buybacks, and purchases of existing assets and not for production actually make Professor Richard Werner’s work of the dis-aggregated theory of credit a much more significant cause of the low growth delivered by each additional unit of debt. and not the energy cost of Energy, Ecoe is a theory whose time has not come and may still not ever arrive.

The problems in Political Economy as they stand presently and the question of future Political Economy based upon future unknown Energy realities are I think helpfully separated which is something Prof. David MacKay is very successful with, in his presentation of the question see the excellent online book, Sustainable energy without hot air.

The Problems are only weakly related with respect to future solutions and breaking the process into 3 parts is useful rather than lumping them all together. It is clear that the existing Form of Market economy and political economy is not able to solve the problem at stage 3 ( I.E Post 2050 post-Oil Economy)

Stage 1 requires a reform of the existing paradigm which involves facing up to the broken debt-based money system. Pension provision, the sovereign debt crisis and Public debt crisis are all addressable and will see improvements even within the deteriorating Cost of energy inputs as a share of output. We could call this stage lets fix what we know is not working.

Stage 2 covers the Post Financialised ( Big Bang Experiment) period to the oil running out in 2050.

This requires a much more long-term investment horizon and complicating the energy mix by overstating the ”Climate Change question** seems to be counterproductive, again I like the way Prof David Mackay dealt with the question including stating the necessities of **Clean Coal and Nuclear”. In this stage, we will be implementing ideas previously barred due to the denial inherent in clinging to a failing system.

Stage 3 Post 2050, This part is much easier than Stage 2 and stage 1, in my opinion, the myth-busting and levelling out inherent in solving the political problems at stage 1 and the challenge to vested interests in stage 2 are by far and away the largest obstacles to getting down to Brass tacks in my opinion.

To Quote Quine, I have in mind his differences of degree and not kind in a way,

this from Two dogmas of empiricism.

´´As an empiricist I continue to think of the conceptual scheme of science as a tool, ultimately, for predicting future experience in the light of past experience. Physical objects are conceptually imported into the situation as convenient intermediaries — not by defnition in terms of experience, but simply as irreducible posits18b comparable, epistemologically, to the gods of Homer. Let me interject that for my part I do, qua lay physicist, believe in physical objects and not in Homer’s gods; and I consider it a scientifc error to believe otherwise.´´

Is the present “Collapse” Managed, Engineered, or an inevitability of Elitist Hubris?

I would argue its a combination of Premature transition management engineering, What’s known as the “Great Reset”

Presently though Central Bank Digital Currencies a new Going Direct solution to the misdiagnosed Banking collapse of the September 2019 New York repo rate spike is being implemented.

“The BlackRock plan calls for blurring the lines between government fiscal policy and central bank monetary policy – exactly what the U.S. Treasury and the Federal Reserve are doing today in the United States. BlackRock has now been hired by the Federal Reserve, the Bank of Canada, and Sweden’s central bank, Riksbank, to implement key features of the plan. Three of the authors of the BlackRock plan previously worked as central bankers in the U.S., Canada and Switzerland, respectively.”

Douthwaite can usefully be consulted in how the monetary system can sensibly be modified or recalibrated to avoid the credit misallocation inherent in the modern monetary regime his short book,The Ecology of Money (Schumacher Briefing, 4) https://az.1lib.to/book/896040/105bf6

Chapter 4: One Country, Four Currencies

“Now we’ve surveyed the various types of the money system, we come to the exciting bit – specifying

the integrated multi-currency system of the future. We have seen that three groups (commercial

institutions, governments and users) can create money. Very little can be said in favour of

allowing the commercial creation of money to continue. Instead, money should be created by

non-profit-seeking organisations representing the people using it. In the case of a democratic

country, this would obviously include a national or regional government working on behalf of its

people.

At least four types of money are needed. One is an international currency, playing the role taken

by gold before the collapse of the gold exchange standard. The second is a national or regional

(sub-national) currency that would relate to the international currency in some way. Thirdly, we

would need a plethora of currencies which, like LETS, the WIR and the commodity-based

currencies, could be created at will by their users to mobilise resources left untapped by national

or regional systems. Many of these user currencies would confine their activities to particular

geographic areas, but some would link non-spatially-based communities of interest. And fourth,

as our current money’s store of value function can so easily conflict with its use as a means of

exchange, special currencies are needed for people wishing to see their savings hold their value

while still keeping them in a fairly liquid form.”

Douthwaite’s briefing has a foreword by Bernard Leitaer.

“Do I agree with all the ideas that are presented here? Even Douthwaite admits that he doesn’t

“expect everyone to agree with the conclusions he has reached”. For instance, although I agree

with him on the importance of linking monetary issues to energy sustainability, I question the

viability of the means he proposes. (Why not include his “Energy-Backed Currency Units”

(ebcu) as part of a basket of commodities and services backing the currency – rather than being

the exclusive backing of currency?”

Leitaers TERRA is easily sourced online.

SEEDS sady has rushed to put the ECOE cart before the usury horse. in Short Seeds is a metric whose day has not and may not come particularly if one follows the science and technology of energy, materials and production.

Stylized modelled theory and Empirical Evidence. Seeds of Proof.

rogerglewis March 4, 2022

Tim, You say and have said before many times that.

“All of these hopes miss the fundamental point, which is that ECoEs are very much higher now (above 9%) than they were in the 1970s (at or below 2%).”

Russian and Saudi Lifting costs account for a very large part of core world supply and also proved reserves for future supply, as the proved reserves are using enhanced recovery methods but not the more expensive heat-based recovery of non-conventional heavy oils. I think the simple claim that a substantial proportion of world oil production and continuing supply from those reserves are still at High ECOEs, can you prove otherwise?

Accessible data available in admittedly partial data sets, contradict the very stark claim you make that up to the 1990’s it cost 2 barrels of oil to extract 100 barrels giving a net 98 surplus energy barrels. and that now the energy cost is 9 barrels of every 100 giving 91 surplus barrels.

Adjusted lifting costs on a per-dollar basis have if anything fallen, it is also possible that for Giant fields that lifting costs have actually fallen in Energy terms.

Are your 2% and 9% figures theoretically or empirically derived and if empirically could you please provide the data source from which you derive such a bold claim?

It is also unsatisfactory not to provide adjusted figures for the different souces be they, conventional Land, off shore, deep sea and shallow and deeper conventional sources.

At this point I think it is reasonable to put the End of cheap oil in energy terms theorists to proof.

This paper tackles the question in energy terms and not assumptions drawn from monetary/price assumptions.

https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4687841/

Discussion

The net energy return ratios (NERs) examined in this study for global oilfields range from approximately 2:1 to 100:1, with a production-weighted mean of 33:1. These results are most sensitive to changes when the gas processing configuration is unknown (as discussed above) or where the properties of injected steam are unknown. The implications of these relative magnitudes of energy returns are robust to explored uncertainties. A resource with an small energy return ratio may face challenges in scaling output, will consume large amounts of energy for production, and likely cause large environmental and climate impacts per unit of energy produced. This range of observed NER ratios is within the range suggested in prior literature. This agreement is a sign of convergence between methodologies: while the method used here is much more specific than prior methods, in that it models the engineering processes in oil extraction in greater detail, it provides similar order of magnitude results as methods used elsewhere.

Here is another comprehensive report

Click to access 60999-EROI_of_Global_Energy_Resources.pdf

What I am getting at is that at best you are in making the claims you do for ECOE that they are Stylised and such not fit for policy prescriptions.

https://en.wikipedia.org/wiki/Giant_oil_and_gas_fields

Giant field production properties and behavior

Comprehensive analysis of the production from the majority of the world’s giant oil fields has shown their enormous importance for global oil production.[10] For instance, the 20 largest oil fields in the world alone account for roughly 25% of the total oil production.

Further analysis shows that giant oil fields typically reach their maximum production before 50% of the ultimate recoverable volume has been extracted.[11] A strong correlation between depletion and the rate of decline was also found in that study, indicating that much new technology has only been able to temporarily decrease depletion at the expense of rapid future decline. This is exactly the case in the Cantarell Field.

rogerglewis

on March 5, 2022 at 2:36 pm said:

Your comment is awaiting moderation.

I agree , hard data is difficult to come by in many cases I think the actual information is protected as State Secrets, and certainly where private interests are concerned as highly sensitive with respect to market competitors.

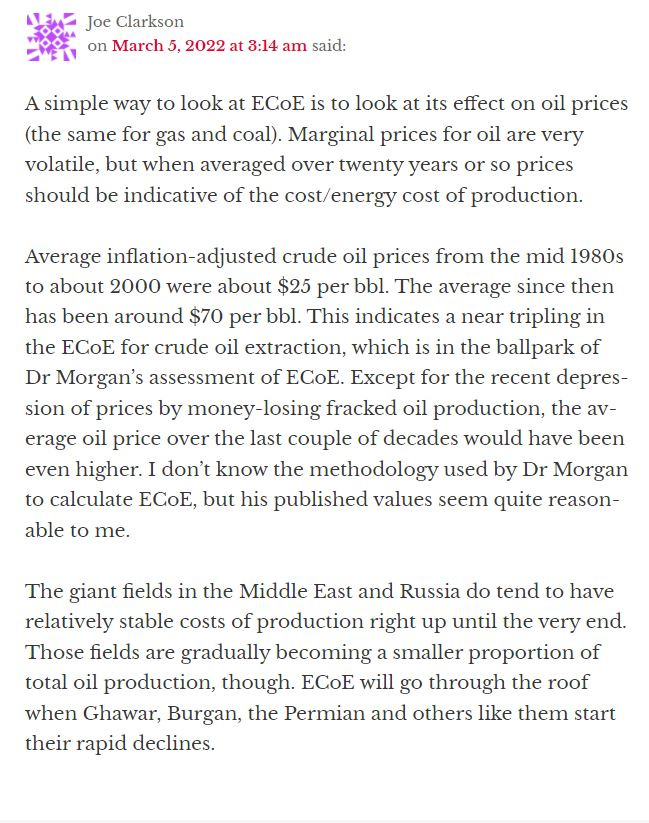

All that said there is data and whilst it should be questioned and analysed, my simple question to Tim is why has he an average ECOE of 1 in 9 out and the Brandt paper from 2015 has a figure of 1 in and 33 out as its average?

https://en.wikipedia.org/wiki/Ghawar_Field

Matthew Simmons, in his 2005 book Twilight in the Desert, suggested that production from the Ghawar field and Saudi Arabia may soon peak.[19]

When appraised in the 1970s, the field was assessed to have 170 billion barrels (27 km3) of original oil in place (OOIP), with about 60 billion barrels (9.5 km3) recoverable (1975 Aramco estimate quoted by Matt Simmons). The second figure, at least, was understated, since that production figure has already been exceeded.[19]

v.

Some sources claim that Ghawar peaked in 2005, though this is denied by the field operators.[8][9]

If you look at fig 2 in the Brandt paper there is enough information to compare the seeds ECOE , assumptions/Data against?

some of the figures suggest that modern deep water rigs produce very competitive ECOE, Girasol in Angola Hibernian in Canada for instance both of which are operated by Oil Majors, is that perhaps a clue regarding who has proprietary technology not available perhaps to say Russia? I really do recommend people look at fig 2 if nothing else.

https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4687841/

rogerglewis

on March 5, 2022 at 1:54 pm said:

Hi Joe,

I am asking for empirical evidence and not proxies for ECOE , EROI is a financial proxy the first study I cited is based on actual lifting costs it suggests that the average actual Energy cost is 1 barrel now to get 33 barrels, a hard number publishes in 2015. Tim is saying that it is 1 barrel gets 9 barrels on average as of now, is this a stylized theoretical claim or empirically based as the Brandt paper is or based upon a differently constituted sampling group?.

The second publication is from 2013 and is based upon EROI measures I must say I think it is more logically consistent and also more empirically robust to consider Mega Joules rather than Dollar ammounts.

the Super Giants will be less than either Tims ECOE average or the brandt paper average I linked to. That the depletion rates of Giant fields have been speculated upon since Hotelling was writing in the 1930’s is a fact I was interested to note that the Brea Olinda field still has the highest ECOE at over 100 and that although it dates from the 1880’s recently consolidation of and sale of wells has been taking place.

https://en.wikipedia.org/wiki/Brea-Olinda_Oil_Field

Peak production on the field was in 1953

Unocal operated most of the field until March 1996, at which time it sold off all of its California assets to Nuevo Energy.[14] Nuevo operated the field for seven years, finally selling its portion of the field in 2003 for $59 million to BlackSand Partners, L.P., prior to themselves being acquired by Plains Exploration & Production.[15] At that time the field was producing 2,269 barrels per day. BlackSand ran operations on the field for a little over three years, and in 2006 Linn Energy bought it from BlackSand for $291 million.[16] In February 2007 Aera Energy LLC transferred its 654 wells on the field to Linn Energy, leaving Linn as the largest operator on the field.[

from fig 2 of Brandt, you will see that Ghwar is given a return of between 35-40 barrels for each barrel expended for lifting costs.

This sort of breakdown of detail is very important when considering realistic policies for the pace and priorities of implementing degrowth policies, or perhaps steady-state policies if one defines the problem slightly more optimistically as I do personally.

Hideawayon March 5, 2022 at 3:44 pm said:

@RogerLewis, as per always, lies, dammed lies and statistics, can say whatever you want them to say if you leave out enough ‘parts’ of the system. The following is from the document you linked ….

“This model does not currently include energy invested in building oilfield capital equipment (e.g., drilling rigs), nor does it include other indirect energy uses such as labor or services.”

“The inclusion of embodied energy in steel and cement consumed would reduce these ERRs by an unknown amount”

Considering the examples are the giants/super giants of the oil industry, which are in decline as a percentage of the total, and smaller fields would have much higher ’embodied energy’ content per produced barrel, then the concept of declining EROEI is very very valid, and likewise the important part of Tim’s thesis, even if the exact number can be debated. It matters not the exact number, just the trajectory, which is clearly demonstrated with things like fracking of shale wells and digging of tar sands.

A common theme from those looking at a utopian future of clean tech is leaving out a lot of very important aspects of the real world to prove their case. For example, and this applies to modern oil fields as much as every other form of new energy, is that the new ‘stuff’ (embodied energy) is always more energy expensive than the existing as the metals used come from mines with lower grades (on average) than those of the past, that take more energy to produce. On average the mines are more remote, with lower grade, deeper and a higher ‘hardness index’ than old mines, because we used all the easy to get high grade metals first!!

Because we are dealing with a huge complex system, going into details would require volumes running into thousands of pages of specifics, where the overall message would get buried in arguments over the detail.

rogerglewis

on March 5, 2022 at 5:08 pm said:

Your comment is awaiting moderation.

Hi Hideaway,

My simple question is where is the empirical data to prove a ECOE of 1 to 9 over the 1 to 33 in the Brandt Paper.

I do not think that Brandt has a dog in the fight to claim lower than 1 to nine or indeed worse.

Your pointing out that embodied energy was not included the calculation, a point which is very clear in the paper’s commentary, will not hugely affect the 1 to 33 ratio not by a factor of 3 in any event.

At another level it is also clear that for the giant fields it would seem that the fixed sunk costs are spread over a longer period of time although it would also seem that Deepwater rigs are also moveable as of course are exploration rigs, there are clearly economies of scale of production that impact on ECOE in some cases and importantly in large fields which are a significant component of core supply, A reading of Stephen J Gould the Median is not the message is recommended in considering weighted sampling.

Perpetual growth is an impossible fantasy – even if we wanted it

18th November 2021 by Tim Morgan 1 Comment

(1)")

As we’ve been reminded at COP-26, climate campaigners believe that the only way in which environmental disaster can be prevented is by the immediate cessation of the use of oil, gas and coal.